We hear the word “payment” from morning to night, but don’t think its easy to master of how its work in backend. It is not just a word it is a sophisticated global field requiring deep expertise to navigate.

Now think about the last time you paid for something online or sent money to a friend. That smooth tap, the “payment successful” ping the instant “Paytm par 501 rupaye prapt hue”. It’s all payments technology working behind the scenes. But what exactly happens when you hit Pay?

If you are a developer curious about fintech, a business owner handling transactions, or just someone who wants to understand modern money movement, this guide breaks it all down.

What A Payment Really is?

A Payment is not something like money moving instantly from one place to another. Better word to define a payment as process.

So how this process looks like:-

- Me Ashish instruct my bank or open my Digital app(Google pay) or wallet or card to pay someone.

- Now this paying process is going through payment rails like Card Networks, bank networks, fintech networks, etc.

- Multiple System check and verify all the basic details to identify risk, fraud, and rules.

- And then Ice-cream owner received money(Paytm par 100 rupaye prapt hue).

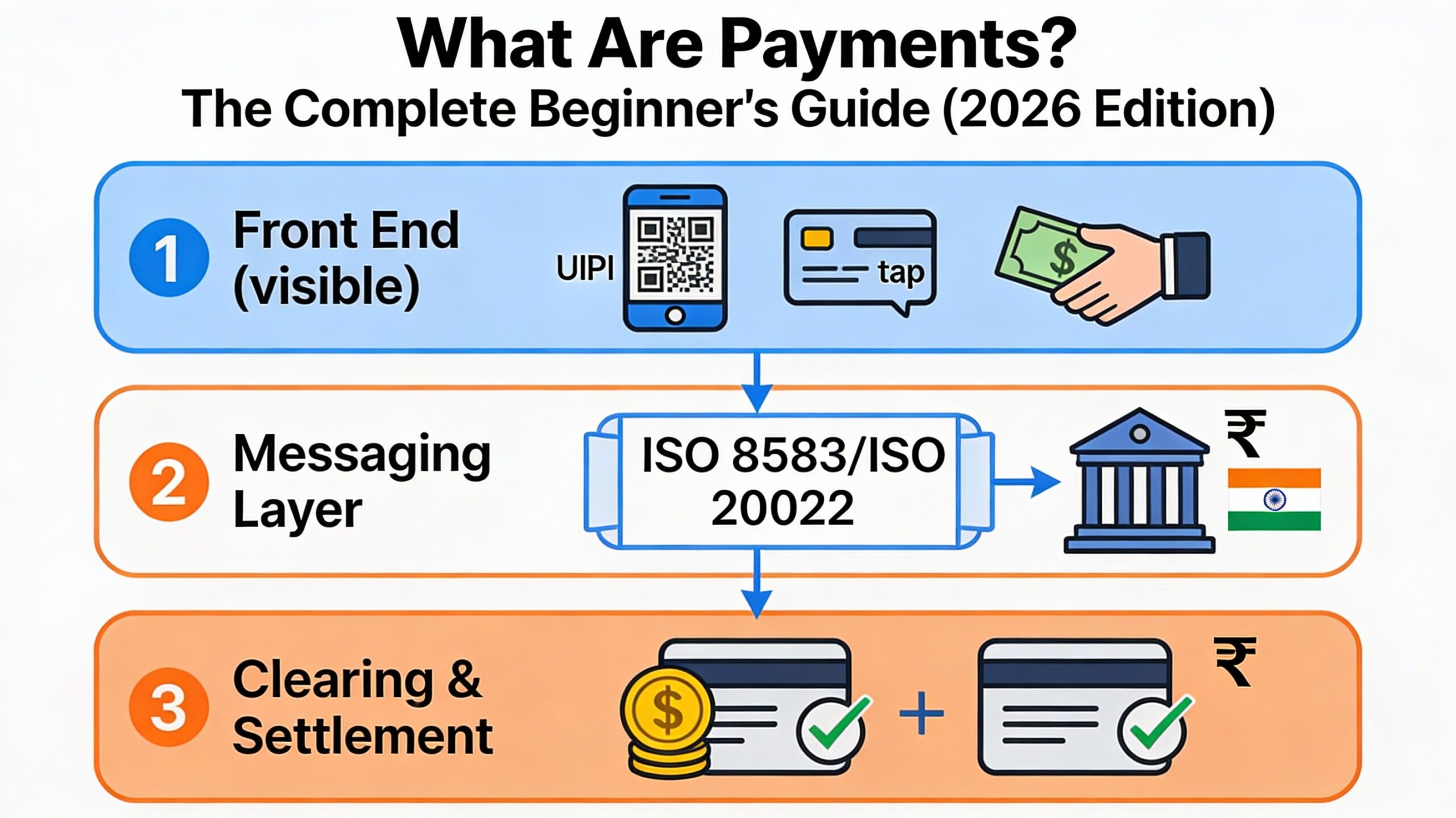

Three Layers of Every Payment

Layering referring here means what a payments processed steps from a customer to bank to receivers.

1. Front End or Visible Things-

Almost everyone on this beautiful planet called earth know about this front end part.

- Cash

- Bank Transfer

- Card Tap

- UPI/QR Scan

- Online checkout

- App-to-app transfer

This is just the front door of the payments process.

2. Messaging/Bank Instruction/ Information-

Every payment you make gets converted into a specific message/file format that banks understand. All the details who’s paying, who’s receiving, the amount, the time, and more are bundled into this structured message. That message is then sent across the payment network to the other bank so they can process and act on it.

For example-

-

For card payments: ISO 8583

-

For modern bank payments: ISO 20022

-

For domestic rails: proprietary formats

- Files also used to inform other banks.

Now the question what information contain in these files or messages.

These messages/files carry:-

-

Who is paying

-

Who is receiving

-

How much

-

Why

-

Risk scoring details

-

Routing info

Messaging/Files/Information is the brain of the payment world.

3. Clearing & Settlement (Where Money Actually Moves)-

This is where actually payments happening basically. In this both counter parties confronted each other and confirm one will debit and other will credit.

Clearing- Bank agree on what happened i.e. who will debit and credit respectively.

Settlement- Now after clearing, Money will be moved between the parties, and actual credit and debit will happen.

Now this question can be asked how often this clearing and Settlement happening. And it depend on payment rail which you have opted for.

Settlement can happen on-

-

Instant

-

Near-instant

-

End-of-day

-

Next-day

Here is one glitch sometime for you as customer the payment looks but actual settlement(money movement happen later).

Parties Involved in Payment Process

There are always 3 parties involved in the payments process

- Payer(me)

- Receiver(Shopkeeper)

- Bank

– Issuer- My bank

– Acquirer- Shop keeper bank

Payment Processor

Payments processors are the mediator of electronic transfer(like credit/debit cars, digital wallets) between payer and receiver’s bank. There are famous example like Stripe, Razorpay, Hayden etc. And now question arise their role and purpose. They basically for business for payments processing and handles following.

-

Transaction routing

-

Risk checks

-

Tokenization

-

Compliance

Payment Rails

I have used payment rails multiple times in this blog. You must wonder what I m referring here. Payment rails are nothing but the digital “highways” or networks that move money from the payer’s bank account to the recipient’s bank account.

For Example- SWIFT, India’s UPI/RTGS/NEFT, US’s ACH, Mexico’s SEPI, Europe SEPA, Brazil’s Pix, Israel’s Zahav etc.

We will deep dive in an other blog about types of payment rails.

Operations and Checks on Payments

While payments processing end to end there are multiple operation happen in the backend which customer don’t know actually but very important for the financial ecosystem.

All the companies or software handle multiple complex operation below:-

-

Fraud checks

-

Anti–money laundering rules

-

Currency conversion

-

Network routing

-

Hardware security modules

-

Chargebacks

-

Risk scoring

-

24/7 uptime

-

Regulatory frameworks

Now see if you pay just $ 1,it involve 8–12 different entities verifying, scoring, approving, and settling.

Payment Trends in 2026

If you are reading till here, then definitely you are someone who have keen interest in payments domain. Now-a-day world is evolving day by day so our payment methods also. If you go back to before 1990 you will not find any digital or electronic transfer by now on one click payments is happening.

The industry is going through its biggest shift in decades. Key trends:

1. Global migration to ISO 20022

This new standard makes transactions richer, faster, and more automated. On this migration we will see multiple articles in upcoming time.

2. Real-time payments becoming the default

Slow transfers are dying out. This is new ear of payment who wants to wait for one day for receiving money in their bank account.

3. Embedded finance everywhere

Apps are becoming mini-banks. This trend is increasing now-a-days across the word. Ex- Buy Now Pay Later

4. AI-driven risk and fraud detection

Legacy rule engines are no longer enough.

5. Cross-border payments finally modernizing

SWIFT, Visa B2B Connect, and blockchain-based rails are reshaping international transfers. Payments in 2026 are faster, smarter, and far more interconnected than ever.

Glitch Payment Failed

This is something all have faced time to time during digital payments. Your first reaction is to blame yourself why me, but most of the time the issue has nothing to do with you. Banks sometimes block normal transactions because their fraud systems get overly cautious. A shop’s payment machine can lose signal for a second. A card chip might not read properly. UPI apps can freeze or timeout. Even big networks have off days. When a payment fails, it’s usually the system, not you. Above are multiple examples why a payment can failed, so next time chill…

Conclusion

Payments seem simple on the surface, but behind each transaction lies a network of rules, signals, checks, and settlement systems working in harmony.

If you understand basics about –

-

the layers

-

the players

-

the rails

-

the messaging/information/files

-

the way money actually moves…then you have a real grasp or understanding of how the financial world works.

Definitely this article give you a sense of how a payments is processed behind the scenes, and and what a payment really is.